Get certified

Our training and certification programs.

1. Certified Basel iii Professional (CBiiiPro), distance learning and online certification program. You can find the program below.

2. Certified Pillar 3 Expert - Basel 3 (CP3E-B3), distance learning and online certification program. You may visit: https://www.basel-iii-association.com/CP3E_B3_Distance_Learning_Online_Certification.html

3. Certified Stress Testing Expert - Basel 3 (CSTE-B3), distance learning and online certification program. You may visit: https://www.basel-iii-association.com/CSTE_B3_Distance_Learning_Online_Certification.html

Certified Basel iii Professional (CBiiiPro), distance learning and online certification program

Overview

Basel III is a comprehensive set of reform measures developed by the Basel Committee on Banking Supervision, to strengthen the regulation, supervision, and risk management of the banking sector.

These measures aim to:

- Improve the banking sector's ability to absorb shocks arising from financial and economic stress, whatever the source;

- Improve risk management and governance;

- Strengthen banks' transparency and disclosures.

Attracting qualified staff is the most important component of any Basel III implementation strategy. Basel III knowledge is one of the main factors that make managers and employees indispensable for financial organizations around the world.

Objectives

The program has been designed to provide with the knowledge and skills needed to understand the Basel III framework, and to work in Basel III projects. The course provides with the skills needed to pass the Certified Basel iii Professional (CBiiiPro) exam.

Target Audience

This course is intended for managers and employees working in banks, financial organizations, financial groups, and financial conglomerates. It is also intended for management consultants, vendors, suppliers, and service providers working for financial organizations.

This course is highly recommended for:

- Managers and professionals involved in Basel III (decision making and implementation),

- Risk and compliance officers,

- Auditors,

- IT professionals,

- Analysts.

Course Synopsis

Introduction.

- What is Basel III?

- Basel III, the G20 and the FSB.

- The Bank for International Settlements (BIS).

- The Basel Committee on Banking Supervision.

- The Basel III Framework.

- National rules implementing Basel III.

The important Basel III Amendments:

Amendment 1. Corporate Governance and Risk Management.

- Sound corporate governance principles.

- a. Board practices.

- b. Senior management.

- c. Risk management and internal controls.

- d. Compensation.

- e. Complex or opaque corporate structures.

- f. Disclosure and transparency.

- The role of supervisors.

Amendment 2. The regulatory capital.

Understanding the Basel III language.

- Securities.

- Debt Securities.

- Bonds.

- Commercial papers.

- Equity securities (common stock).

- Preferred stock.

- Cumulative preferred stock.

- Contingent convertibles (CoCos).

- Perpetual and non-perpetual preferred stocks.

- Paid-up capital.

- Undisclosed reserves.

- Subordinated debt.

- Stock surplus (share premium).

- Hybrid capital instruments.

- Comprehensive income.

- Other comprehensive income (OCI).

- Accumulated other comprehensive income (AOCI).

- Retained earnings.

- Intangible assets.

- Step-up provisions.

- Going concern.

- Gone concern.

- Risk Weighted Assets (RWA).

- Deferred tax.

- Securitisation.

- Resecuritisation.

Capital, the numerator.

- A strict definition of capital.

- 1. Tier 1 Capital (going-concern capital).

- 1a. Common Equity Tier 1 (CET1).

- 1b. Additional Tier 1 (AT1).

- 2. Tier 2 Capital (gone-concern capital).

- Limits and Minima.

- Understanding Common Equity Tier 1 capital.

- Common Equity Tier 1, the 14 criteria.

- Criteria for inclusion in Additional Tier 1 capital.

- Criteria for inclusion in Tier 2 Capital.

- Common shares issued by consolidated subsidiaries.

- Tier 1 and Tier 2 qualifying capital issued by consolidated subsidiaries.

- Regulatory adjustments.

- Double gearing.

- Disclosure requirements.

- Non-viability.

Amendment 3. The Risk Weighted Assets (RWA), the denominator.

- Enhanced risk coverage.

- The RWA after the December 2017 Basel III reforms.

- The 2017 reforms concentrate on the RWAs (the denominator).

Amendment 4. The Capital Ratio.

- The 4.5% and the 7% common equity ratio.

Amendment 5. Credit Risk after December 2017.

- The standardised approach (SA) for credit risk.

- The internal ratings-based (IRB) approaches.

- a. The Foundation IRB (F-IRB).

- b. The Advanced IRB (A-IRB).

- Standardised approach for credit risk.

- The new due diligence requirements.

- Exposures to sovereigns.

- Exposures to non-central government public sector entities (PSEs).

- Exposures to multilateral development banks (MDBs).

- Exposures to banks.

- (a) External Credit Risk Assessment Approach (ECRA).

- (b) Standardised Credit Risk Assessment Approach (SCRA).

- Exposures to covered bonds.

- Exposures to securities firms and other financial institutions.

- Exposures to corporates.

- Specialised lending.

- Subordinated debt, equity and other capital instruments.

- Retail exposures.

- Off-balance sheet items.

- Defaulted exposures.

- Recognition of external ratings by national supervisors.

- Credit risk mitigation (CRM) techniques.

- Collateralised transactions.

December 2017 – Internal ratings-based (IRB) approach for credit risk.

- Unexpected losses (UL), expected losses (EL).

- Categorisation of exposures.

- Asset classes.

- (a) corporate,

- (b) sovereign,

- (c) bank,

- (d) retail, and

- (e) equity.

- Adoption of the IRB approach for asset classes.

- December 2017, stress tests used in assessment of capital adequacy.

Amendment 6. Operational Risk after December 2017.

- Reputational risk.

- Systemic risk.

- Strategic risk.

- The standardised approach methodology.

- The Business Indicator (BI).

- The Business Indicator Component (BIC).

- Regulatory determined marginal coefficients.

- The Internal Loss Multiplier (ILM).

- The BI=ILDC+SC+FC formula.

- The standardised approach operational risk capital requirement.

- Application of the standardised approach within a group.

- General criteria on loss data identification, collection and treatment.

- Specific criteria on loss data identification, collection and treatment.

- Disclosures.

Amendment 7. Global Liquidity Standards.

- Principles for Sound Liquidity Risk Management and Supervision.

The Liquidity Coverage Ratio (LCR).

- Amendments to the LCR.

- The stock of high-quality liquid assets.

- Level 1 assets.

- Level 2 assets.

- Level 2B assets.

- Total net cash outflows.

The Net Stable Funding Ratio (NSFR).

- Available Stable Funding (ASF).

- ASF factors.

- Required Stable Funding (RSF)

- RSF factors.

Monitoring tools.

- a. Contractual maturity mismatch.

- b. Concentration of funding.

- c. Available unencumbered assets.

- d. LCR by significant currency.

- e. Market-related monitoring tools.

- Differences in home / host liquidity requirements.

- Guidance for Supervisors on Market-Based Indicators of Liquidity.

- Liquidity Coverage Ratio Disclosure Standards.

Amendment 8. The Capital Conservation Buffer.

- Distribution policies inconsistent with capital conservation.

- The restriction of dividends and bonuses.

- The buffer of risk-weighted assets.

Amendment 9. The Countercyclical Capital Buffer.

- What is procyclical and countercyclical.

- The buffer.

- Guidance for national authorities operating the countercyclical capital buffer.

- Principles underpinning the role of judgement.

- Jurisdictional reciprocity.

Amendment 10. The Leverage Ratio.

- The Basel III leverage ratio framework.

- The scope of the leverage ratio.

- The ratio.

- (a) On-balance sheet exposures.

- (b) Derivative exposures.

- (c) Securities financing transaction exposures.

- (d) Off-balance sheet (OBS) items.

- Disclosure requirements.

- Disclosure templates.

- The leverage ratio after December 2017.

- The leverage ratio buffer for global systemically important banks (G-SIBs).

- Implementation and monitoring.

Amendment 11. Systemically Important Financial Institutions (SIFIs).

- The additional degree of loss absorbency.

- Lists of global systemically important banks (G-SIBs).

- Updated assessment methodology and the higher loss absorbency requirement.

- a. The size of banks.

- b. Their interconnectedness.

- c. The lack of readily available substitutes or financial institution infrastructure for the services they provide.

- d. Their global (cross-jurisdictional) activity.

- e. Their complexity.

Amendment 12. Risk Modelling, Stress Testing and Scenario Analysis.

- Value-at-risk (VaR).

- Standard Normal Distribution.

- VaR shortcomings.

- Capture of systemic risk/tail events in stress testing and risk modelling.

Amendment 13. Stressed Value-at-Risk (S-VaR), Counterparty Credit Risk (CCR), Credit Valuation Adjustment (CVA).

- Stressed Value-at-Risk (S-VaR).

- Stressed VaR merges stress testing with VaR.

- A stochastic process, a deterministic process.

- Simulations.

- Monte Carlo Simulation.

- The Turner Review, four categories of problems.

- Counterparty Credit Risk (CCR).

- Credit Valuation Adjustment (CVA).

- The adjustments to transaction valuation, to reflect the counterparty’s credit quality.

- One-sided CVA, two-sided CVA.

- CVA Risk Capital Charge.

- Monte Carlo Simulation and CVA.

- CVA after December 2017.

Amendment 14. The output floor (December 2017 update).

- Reducing excessive variability of risk-weighted assets.

- Output floor requirements.

- Calculation of the output floor.

- Disclosure requirements.

- Implementation date and transitional measures.

Islamic Banking and Basel III.

(There are no exam questions from this part).

- Basel III was not designed for Institutions offering Islamic Financial Services (IIFS).

- The Basel III equivalent rules.

- The Islamic Financial Services Board (IFSB).

- The IFSB standards that implement Basel III equivalent rules.

- The Islamic Financial Stability Forum (IFSF).

- The International Islamic Liquidity Management Corporation (IILM).

- The Islamic Development Bank (IDB).

- The Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI).

- Understanding Profit-sharing investment accounts (PSIAs).

- Musharakah and Mudarabah partnerships.

- IFSB 1 - Guiding Principles of Risk Management.

- IFSB 12 - Guiding Principles on Liquidity Risk Management.

- IFSB 13 - Guiding Principles on Stress Testing.

- IFSB 15 - Revised Capital Adequacy Standard.

- IFSB 16 - Revised Guidance on Key Elements In The Supervisory Review Process.

- IFSB 17 - Core Principles for Islamic Finance Regulation (Banking Segment) (CPIFR).

- IFSB 19 - Guiding Principles on Disclosure Requirements.

Closing remarks.

Become a Certified Basel iii Professional (CBiiiPro)

We will send the program up to 24 hours after the payment. Please remember to check the spam folder of your email client too, as emails with attachments are often landed in the spam folder.

You have the option to ask for a full refund up to 60 days after the payment. If you do not want one of our programs or services for any reason, all you must do is to send us an email, and we will refund the payment, no questions asked.

Your payment will be received by our strategic partner and service provider, Cyber Risk GmbH (Dammstrasse 16, 8810 Horgen, Switzerland, Handelsregister des Kantons Zürich, Firmennummer: CHE-244.099.341). Cyber Risk GmbH may also send certificates to all members.

The all-inclusive cost is $297. There is no additional cost, now or in the future, for this program.

First option: You can purchase the Certified Basel iii Professional (CBiiiPro) program with VISA, MASTERCARD, AMEX, Apple Pay, Google Pay etc.

Purchase the CBiiiPro program here (VISA, MASTERCARD, AMEX, Apple Pay, Google Pay etc.)Second option: QR code payment.

i. Open the camera app or the QR app on your phone.

ii. Scan the QR code and possibly wait for a few seconds.

iii. Click on the link that appears, open your browser, and make the payment.

Third option: You can purchase the Certified Basel iii Professional (CBiiiPro) program with PayPal

When you click "PayPal" below, you will be redirected to the PayPal web site. If you prefer to pay with a card, you can click "Debit or Credit Card" that is also powered by PayPal.

What is included in the program:

A. The official presentations (1,557 slides)

There are 355 additional slides that cover Islamic banking and Basel III (there are no exam questions from this part).

The presentations are effective and appropriate to study online or offline. Busy professionals have full control over their own learning and are able to study at their own speed. They are able to move faster through areas of the course they feel comfortable with, but slower through those that they need a little more time on.

B. Up to 3 online exam attempts per year

Candidates must pass only one exam to become CBiiiPros. If they fail, they must study the official presentations and retake the exam. Candidates are entitled to 3 exam attempts every year.

If candidates do not achieve a passing score on the exam the first time, they can retake the exam a second time.

If they do not achieve a passing score the second time, they can retake the exam a third time.

If candidates do not achieve a passing score the third time, they must wait at least one year before retaking the exam. There is no additional cost for any additional exam attempts.

To learn more, you may visit:

https://www.basel-iii-association.com/Questions_About_The_Certification_And_The_Exams_1.pdf

https://www.basel-iii-association.com/Certification_Steps_CBiiiPro.pdf

C. The Certificate, with a scannable QR code for verification.

You will receive your certificate via email in Adobe Acrobat format (pdf), with a scannable QR code for verification, 7 business days after you pass the exam. A business day refers to any day in which normal business operations are conducted (in our case Monday through Friday), excluding weekends and public holidays.

D. One web page of the Basel iii Compliance Professionals Association (BiiiCPA) dedicated to you (https://www.basel-iii-association.com/Your_Name.htm).

When third parties scan the QR code on your certificate, they will visit the web page of the Basel iii Compliance Professionals Association (BiiiCPA) that is dedicated to you. They will be able to verify that you are a certified professional, and your certificates are valid and legitimate.

In this dedicated web page we will have your name, the certificates you have received from us, pictures of your certificates, and a picture of your lifetime membership certificate if you are a lifetime member.

This is an example: https://www.basel-iii-association.com/John_Anderson.htm

Professional certificates are some of the most frequently falsified documents. Employers and third parties need an easy, effective, and efficient way to check the authenticity of each certificate. QR code verification is a good response to this demand.

Frequently Asked Questions

1. I want to learn more about the Basel iii Compliance Professionals Association (BiiiCPA).

The Basel iii Compliance Professionals Association (BiiiCPA) is the largest association of Basel iii Professionals in the world. It is a business unit of the Basel ii Compliance Professionals Association (BCPA), the largest association of Basel ii Professionals in the world.

The BiiiCPA is a global community of experts working in risk and compliance management, that explore career avenues, and acquire lifelong skills.

Both associations are wholly owned by Compliance LLC, a company incorporated in Wilmington, NC, and offices in Washington, DC, a provider of risk and compliance training and executive coaching in 57 countries.

Several business units of Compliance LLC are very successful associations that offer standard, premium and lifetime membership, weekly or monthly updates, training, certification, Authorized Certified Trainer (ACT) programs, interest representation, and other services to their members. The business units of Compliance LLC include:

- The Sarbanes-Oxley Compliance Professionals Association (SOXCPA), the largest Association of Sarbanes-Oxley professionals in the world. You may visit: https://www.sarbanes-oxley-association.com

- The Solvency II Association, the largest association of Solvency II professionals in the world. You may visit: https://www.solvency-ii-association.com

- The International Association of Risk and Compliance Professionals (IARCP). You may visit: https://www.risk-compliance-association.com

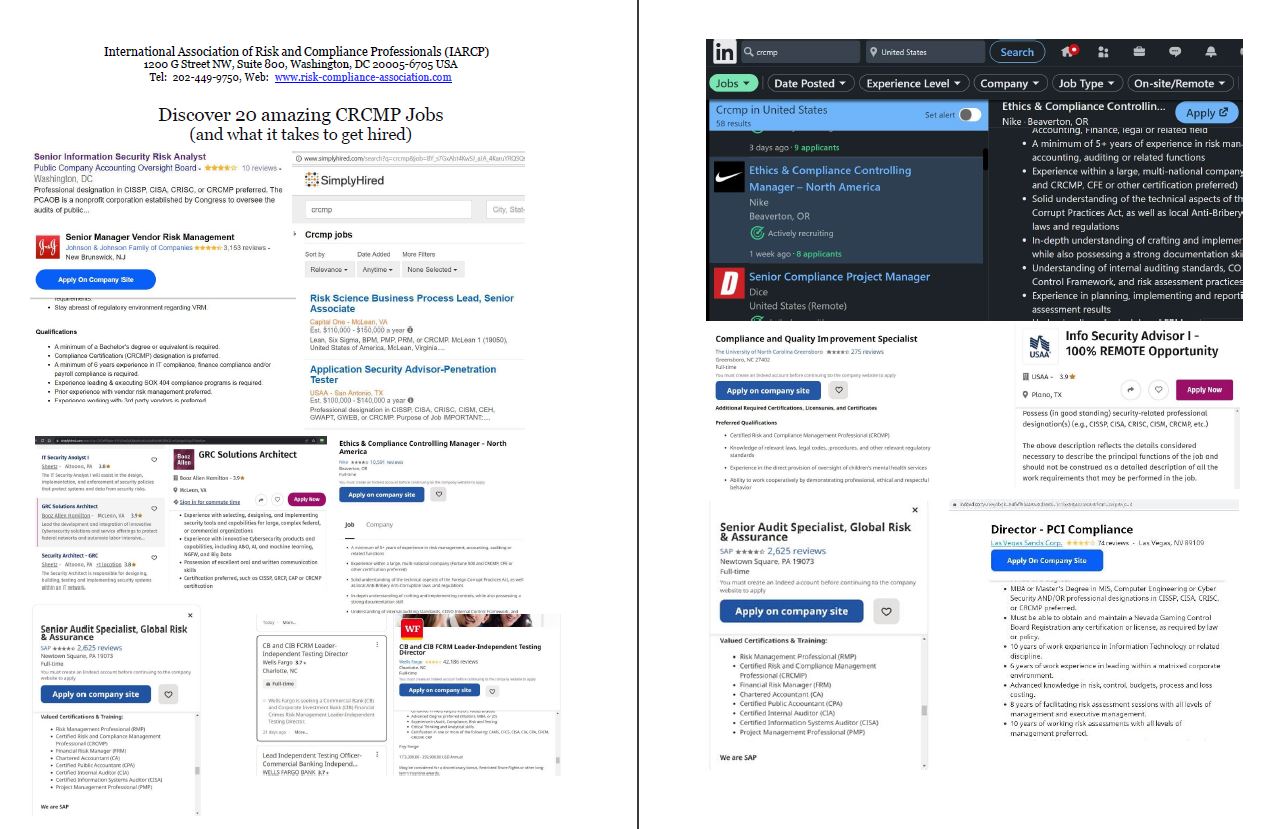

The Certified Risk and Compliance Management Professional (CRCMP) certificate, from the IARCP, has become one of the most recognized certificates in risk management and compliance. There are CRCMPs in 57 countries. Companies and organizations around the world consider the CRCMP a preferred certificate.

You can find more about the demand for CRCMPs at: https://www.risk-compliance-association.com/CRCMP_Jobs_Careers.pdf

2. Does the association offer training?

The BiiiCPA offers distance learning and online certification programs in most countries, and in-house instructor-led training programs in companies and organizations in many countries.

A. Distance learning and online certification programs.

- Certified Basel iii Professional (CBiiiPro). To learn more, you may visit: https://www.basel-iii-association.com/Basel_III_Distance_Learning_Online_Certification.html

- Certified Pillar 3 Expert - Basel 3 (CP3E-B3). To learn more, you may visit: https://www.basel-iii-association.com/CP3E_B3_Distance_Learning_Online_Certification.html

- Certified Stress Testing Expert - Basel 3 (CSTE-B3). To learn more, you may visit: https://www.basel-iii-association.com/CSTE_B3_Distance_Learning_Online_Certification.html

B. Instructor-led training.

The association develops and maintains three certification programs and many tailor-made training programs for directors, executive managers, risk and compliance managers, internal and external auditors, data owners, process owners, consultants, suppliers, and service providers.

For instructor-led training, you may contact Lyn Spooner at: lyn@basel-iii-association.com

3. Is there any discount available for the distance learning programs?

We do not offer a discount for your first program, as we want to keep the cost as low as possible for all members. You have a $100 discount for your second and each additional program.

For example, after you purchase the Certified Basel iii Professional (CBiiiPro) program at $297, you can purchase:

- The Certified Pillar 3 Expert - Basel 3 (CP3E-B3) program at $197 (instead of $297).

- The Certified Stress Testing Expert - Basel 3 (CSTE-B3) program at $197 (instead of $297).

- The Certified Risk and Compliance Management Professional (CRCMP) program at $197 (instead of $297),

- The Certified Information Systems Risk and Compliance Professional (CISRCP) program at $197 (instead of $297),

- The Certified Cyber (Governance Risk and Compliance) Professional - CC(GRC)P program at $197 (instead of $297),

- The Certified Risk and Compliance Management Professional in Insurance and Reinsurance - CRCMP(Re)I program at $197 (instead of $297),

To find more about programs 3 to 6 above, you may visit the International Association of Risk and Compliance Professionals (IARCP) at: https://www.risk-compliance-association.com/Distance_Learning_and_Certification.htm

Lifetime members can purchase each of the distance learning and online certification programs at $148, instead of $297.

If you are a lifetime member, or you have already purchased one of our programs and you want to purchase your next discounted program, you can contact Lyn Spooner via email to receive the URL for the discounter price (at lyn@basel-iii-association.com).

4. Are your training and certification programs vendor neutral?

Yes. We do not promote any products or services, and we are 100% independent.

5. Are there any entry requirements or prerequisites required for enrolling in the training programs?

There are no entry requirements or prerequisites for enrollment. Our programs give the opportunity to individuals of all levels to learn, grow, and develop new skills without the need for prior qualifications or specific experience.

6. I want to learn more about the exam.

You can take the exam online from your home or office, in all countries.

It is an open book exam. Risk and compliance management is something you must understand and learn, not memorize. You must acquire knowledge and skills, not commit something to memory.

You will be given 90 minutes to complete a 35-question exam. You must score 70% or higher.

The exam contains only questions that have been clearly answered in the official presentations.

All exam questions are multiple-choice, composed of two parts:

a. A stem (a question asked, or an incomplete statement to be completed).

b. Four possible responses.

In multiple-choice questions, you must not look for a correct answer, you must look for the best answer. Cross out all the answers you know are incorrect, then focus on the remaining ones. Which is the best answer? With this approach, you save time, and you greatly increase the likelihood of selecting the correct answer.

TIME LIMIT - This exam has a 90-minute time limit. You must complete this exam within this time limit, otherwise the result will be marked as an unsuccessful attempt.

BACK BUTTON - When taking this exam you are NOT permitted to move backwards to review/change prior answers. Your browser back button will refresh the current page instead of moving backward.

RESTART/RESUME – You CANNOT stop and then resume the exam. If you stop taking this exam by closing your browser, your answers will be lost, and the result will be marked as an unsuccessful attempt.

SKIP - You CANNOT skip answering questions while taking this exam. You must answer all the questions in the order the questions are presented.

We do not send sample questions or past exams. If you study the presentations, you can score 100%.

When you are ready to take the CBiiiPro exam, you must follow the steps: https://www.basel-iii-association.com/Certification_Steps_CBiiiPro.pdf When you are ready to take the CP3E-B3 exam, you must the steps: https://www.basel-iii-association.com/Certification_Steps_CP3E_B3.pdf When you are ready to take the CSTE-B3 exam, you must follow the steps: https://www.basel-iii-association.com/Certification_Steps_CSTE_B3.pdf7. How comprehensive are the presentations? Are they just bullet points?

The presentations are not bullet points. They are effective and appropriate to study online or offline.

8. Do I need to buy books to pass the exam?

No. If you study the presentations, you can pass the exam. All the exam questions are clearly answered in the presentations. If you fail the first time, you must study more. Print the presentations and use Post-it to attach notes, to know where to find the answer to a question.

9. Is it an open book exam? Why?

Yes, it is an open book exam. Risk and compliance management is something you must understand and learn, not memorize. You must acquire knowledge and skills, not commit something to memory.

10. Do I have to take the exam soon after receiving the presentations?

No. You can take the exam any time. Your account never expires. You have lifetime access to the training program. If there are any updates to the training material, the updated program will be sent free of charge.

11. Do I have to spend more money in the future to remain certified?

No. Your certificate never expires. It will be valid, without the need to spend money or to take another exam in the future.

12. Ok, the certificate never expires, but things change.

Recertification would be a great recurring revenue stream for the association, but it would also be a recurring expense for our members. We resisted the temptation to "introduce multiple recurring revenue streams to keep business flowing", as we were consulted. No recertification is needed for our programs.

Things change, and this is the reason you need to become (at no cost) a member of the association. Every month you can visit the "Reading Room" of the association and read our newsletter with updates, alerts, and opportunities, to stay current.

13. How many hours do I need to study to pass the exam?

You must study the presentations at least twice, to ensure you have learned the details. The average time needed is:

- 42 hours for the CBiiiPro program,

- 17 hours for the CP3E-B3 program,

- 33 hours for the CSTE-B3 program.

This is the average time needed. There are important differences among members.

14. I want to receive a printed certificate. Can you send me one?

Unfortunately this is not possible. You will receive your certificate via email in Adobe Acrobat format (pdf), with a scannable QR code for verification, 7 business days after you pass the exam. A business day refers to any day in which normal business operations are conducted (in our case Monday through Friday), excluding weekends and public holidays.

The association will develop a dedicated web page for each certified professional (https://www.basel-iii-association.com/Your_Name.html). In your dedicated web page we will add your full name, all the certificates you have received from the association, and the pictures of your certificates.

When third parties scan the QR code on your certificate, they will visit your dedicated web page, and they will be able to verify that you are a certified professional, and your certificates are valid and legitimate.

Professional certificates are some of the most frequently falsified documents. Employers and third parties need an easy, effective, and efficient way to check the authenticity of each certificate. QR code verification is a good response to this demand.

You can print your certificate that you will receive in Adobe Acrobat format (pdf). With the scannable QR code, all third parties can verify the authenticity of each certificate in a matter of seconds.

15. Which is the refund policy?

The association has a very clear refund policy: You have the option to ask for a full refund up to 60 days after the payment. If you do not want one of our programs or services for any reason, all you must do is to send us an email, and we will refund the payment after one business day, no questions asked.

16. Why should I get certified, and why should I choose your certification programs?

- The Basel iii Compliance Professionals Association (BiiiCPA) is the largest association of Basel iii Professionals in the world. It is a business unit of the Basel ii Compliance Professionals Association (BCPA), the largest association of Basel ii Professionals in the world.

- Our training programs are flexible and convenient. Learners can access the course material and take the exam at any time and from any location. This is especially important for those with busy schedules.

- The all-inclusive cost of our programs is very low. There is no additional cost for each program, now or in the future, for any reason.

- If you purchase a second program, you have a $100 discount. The all-inclusive cost for your second (and each additional) program is $197.

- There are 3 exam attempts per year that are included in the cost of each program, so you do not have to spend money again if you fail.

- No recertification is required. Your certificates never expire.

- The marketplace is clearly demanding qualified professionals in risk and compliance management. Certified professionals enjoy industry recognition and have more and better job opportunities. It is important to get certified and to belong to professional associations. You prove that you are somebody who cares, learns, and belongs to a global community of professionals.

- Firms and organizations hire and promote fit and proper professionals who can provide evidence that they are qualified. Employers need assurance that managers and employees have the knowledge and skills needed to mitigate risks and accept responsibility. Supervisors and auditors ask for independent evidence that the process owners are qualified, and that the controls can operate as designed, because the persons responsible for these controls have the necessary knowledge and experience.

- Professionals that gain more skills and qualifications often become eligible for higher-paying roles. Investing in training can have a direct positive impact on a manager's or employee's earning potential.

BiiiCPA, some of our clients